Managing cash flow control in construction projects entails planning of fund utilization, monitoring of budget implementation and evaluation of results. Since funding comes from clients, proper utilization and adequate cash inflow are factors that affect the profitability of a construction project.

Important Aspects of Cash Flow Management in Construction Projects

Managing cash flow control in construction projects is an important aspect of project management’s plan execution. Cost and funding problems usually arise from a chain of activities. To ensure the project’s continuity, this should be recognized by a system of procedures that recognizes the existence of deviations and their extent.

A set of project control processes for managing cash flow in construction projects is not intended for cost-savings objectives because this aspect should have been achieved at the planning stage. The focus of cash flow control is to fulfill what was originally planned because major changes if any, have already been anticipated and covered during the formulation of said plan.

The focal points of this article are the resource documents for cash utilization, as well as the accounting records and tools for monitoring. The purpose is to recognize and identify the deviations from where and when cost problems arise.

I. Developing the Budget for Utilization Control

Construction projects are expense-oriented undertakings; hence, the importance of having a project budget should never be underrated. They may be cost estimates, but the manner by which such estimates have been established should be thoroughly planned and laid out.

The project budget and the projected cash flow are essential because the final estimates shall serve as the baseline reference against which actual expenses are monitored. That way, the manager will recognize overruns and their potential for becoming cost control problems and the extent by which they can affect the ongoing construction project.

Important Considerations of a Project Budget

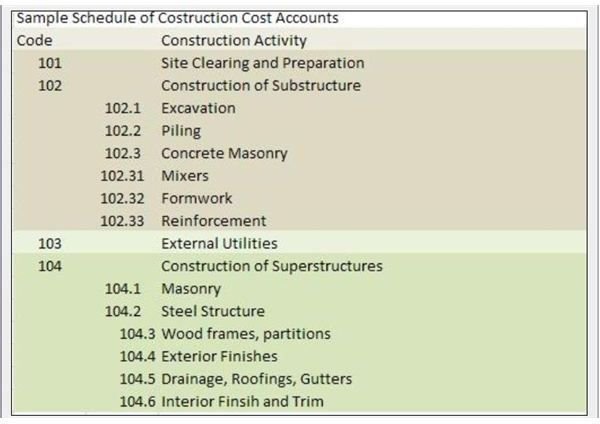

1) Identifying the Cost Accounts

Estimating the cost of a construction project involves the preparation of a checklist containing all the transactions, scheduled or listed according to the project plan. Cost accounts are identified and are segregated according to the types of activity where the materials are needed, the equipment required, the manpower costs and such other similar aspects whether physical or non-physical accounts. Examples of non-physical accounts are interest charges, rental expenses, taxes, consultation fees, etc.

2) Developing a Schedule of Cost Accounts

Identifying the costs is one thing; the matter of communicating these costs to all parties involved in carrying out the project plan is another. What may be clearly defined to the planner could be vague or a gray matter to the site foreman or to the procurement manager.

A coding system that assigns a specific number to a particular cost account should always be a point of reference for communicating information. This ensures that the communicator and the recipient of the information or instructions are referring to the same cost item.

Construction projects can have as much as 400 cost accounts that could be identified; hence all such expenditures should be coded accordingly and in relation to the activity category.

Let’s say the construction project is to be divided into four phases or stages; then there has to be a list that assigns 100 expense accounts for each construction stage. This could mean that the first stage has an assigned numeric code that begins from 01-100 to readily indicate that these are expense accounts related to the initial phase of the project plan. It follows that the second stage will be numbered from 101 to 200 and so forth, which is regardless whether the entire set of 100 numbers is used or not.

The screenshot image on your left illustrates how project costs are identified and numerically coded.

3) Making a Forecast Estimate

In managing cash flow control in a construction project, the deviations in project costs are anticipated at the time of developing the budget plan. These are referred to as contingency costs , and are based on historical costs plus a reasonable estimate of price inflation based on current market conditions.

In making a forecast for estimates, the project manager and accountant make use of previous reports as baseline reference. In some cases, a more up-to-date reference would be a similar project that is currently ongoing; in which case, the current job status report provides the budget planner with a more accurate estimate for price inflation.

Find out how this forecast is estimated on page 2 of Cash Flow Control in Construction Projects.

3) Making a Forecast Estimate (continued)

Simple Forecasting Method:

A straightforward method for managing cash flow control in construction projects is one where the planner simply calculates the 100% equivalent cost of a completed activity.

Technically, the formula for calculating uses Ct as the cost to date, and Pt as the proportion of work completed to date; then Cf would be the forecast cost. The formula would be Cf = Ct / Pt.

To illustrate:

Supposing a similar activity is forty-two percent (42%) complete and the total cost to date is $40,000, then the cost estimate to forecast is calculated as follows:

Cost Estimate = $40,000 / 0.42 = $95,240

Forecasting Based on Number of Work Units

If a given activity is scheduled to be completed within 180 days and the average cost per unit incurred was computed at $255 per day, then the estimated cost is computed as follows:

Cost Estimate = 180 days to complete x $255 per day = $45,900

However, if a work-associated problem is to be recognized, in which the work in progress is expected to improve during the succeeding periods, then the formula will be modified accordingly. The planner determines how much of the work remains, and multiplies the result by the average cost of work per unit.

To illustrate:

Supposing current costs to date of $8,570 have been incurred for 25 days, while the total cost estimate is $40,000. However, there were some problems encountered during the 25 days and the site engineer gave information that work flow has returned to normal. The project therefore is expected to proceed as planned. The cost estimate will then be computed as follows:

Average Cost per Unit of Work = $40,000 / 180 days = $222

Work days remaining = 180 days – 25 days = 155

Cost Estimate = Cost to date + (Work days remaining x Cost of Work per unit)

Cost Estimate = $8,570 + (155 days x $222)

Cost Estimate = $8,570 + $34,410

Cost Estimate = $43,160

There are other factors that could influence the cost estimation , yet the essence of taking into account the changes will relatively be according to the same methods as above. The important factor is that the inputs for the budget plan shall integrate forecasts of possible problems such as overruns and price inflation for every activity.

In managing the cash flow control in construction projects, greater emphasis is placed in the development of cost control guidelines and not cost-saving measures, especially for building constructions. This is one undertaking where quality should never be sacrificed for economy for obvious reasons.

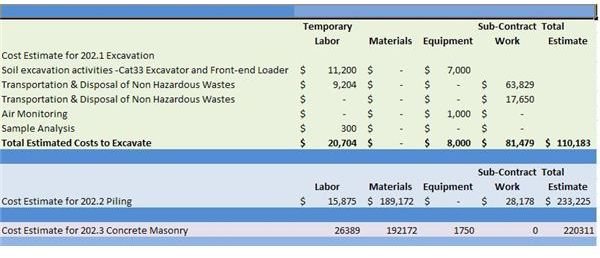

4) Converting the Cost Estimates into a Budget Plan

As mentioned earlier, the cost accounts are to be segregated according to the function as they appear in the project plan. This stands opposed to financial cost accounting where segregations are based on the nature of the expense, i.e. material, labor, utilities. Nevertheless, these expenses should be provided with summary totals in case there is the need to determine their aggregate costs individually.

The project’s budget plan integrates the materials, the labor, the utilities and all other related expenses to a particular function or task to be performed.

To illustrate, click on the image on your left for a larger view of how Costs 202.1 (cost of excavation), 202.2 (cost of piling) and 202.3 (cost of concrete masonry) were provided with cost estimates before they were converted into project costs. Take note of how labor, materials, equipment cost and sub-contract work were integrated as a single cost account.

Proceed to the next page where this article about managing cash flow control in construction projects delves into the cash flow status report.

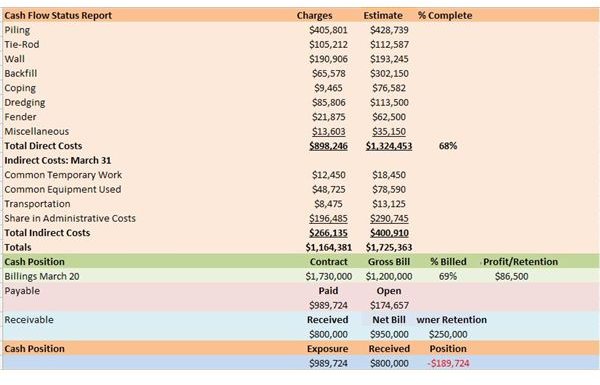

II. Monitoring the Budget Implementation - Cash Flow Status Report

Managing the cash flow control of a construction project requires the monitoring of cash collections and utilization, which can be gleaned from the cash flow status report. There are no hard rules on how this report is presented but the main objective is to determine the current cash position of the project funds. Hence this should be the baseline figure.

Click on the screenshot image on your left to view a larger image of a sample cash flow status report.

The Total Costs

Costs incurred and estimated are presented into two sections: the Direct Costs and the Indirect Costs . View the sample where the actual costs are compared against the estimate for the said activity; hence the percentage of completion is computed by dividing the total actual charges over the total estimate ($898,246 / $1,324,453), which is 68%.

The project manager has to consider the company’s administrative and other overhead costs for determining the costs related to the completed portion of the construction project. Hence, the total cash output to date is $1,164,381.

Billings

Glean from this section the amount of the contract price and how much has been billed to the building owner. The construction company has integrated its 5% retention profit in the amount of the contract price. Take note that sixty-nine percent (69%) has been billed to the client, for which the amount of the expected profit to be realized at this stage should be $86,500. That applies if the client actually pays the billed amount.

Payable:

Not all charges will be reported as actual cash outlay, since some may still be unpaid as of report date. You can find out why by taking a look at the amount of receivables.

Receivable:

Understand the title “Net Bill” is different from the concept of “Gross Bill”. Although the client has been billed, it is possible that payment is still being processed or a certain portion was intentionally retained by the owner.

In this sample, the owner was already billed the amount of $1,200,000 representing sixty-nine percent (69%) of the costs to cover for sixty-eight percent (68%) job completion. However, the construction company actually received $800,000 only. Instead of retaining a profit of $60,000 ($1,200,000 x 5%), the company stands to gain only $40,000 ($800,000 x 5%) as of report date. .

However, for some reason, the owner decided to reduce the payment by $250,000; hence the construction company is bound to receive only $950,000. This means that the company’s total exposure of $1,164,381 is not yet paid in full by the owner. Hence, some of the accounts payable ($174,657) remain unpaid as of the cash flow date, while the construction company’s profits as of the report date have not yet been realized.

The cash flow report shows that the billing amount and percentage of completed project do not stray far from each other; but the cash position of the company is affected by the slow payment of the client-owner.

Cash Flow Control in Construction Projects concludes on page 4.

III. Evaluating the Financial Reports

The project’s budget plan and cash flow status report are only two of the baseline references used for managing the cash flow control of an ongoing construction project. Financial reports likewise provide the financial summary of how the ongoing construction activities are affecting the company’s current financial position.

Information from the income statement and balance sheet report provides project managers with overviews about the components that make up the company’s liquid position. Understanding the ratios about liquidity and debt-to-equity ratio will give the project manager insights about the company’s financial capabilities. Ratios for accounts receivable and accounts payable turnovers reflect the collection and payment activities and their effects on liquidity.

The income and expenses relate to how much cash has been generated from construction projects and the costs incurred by the company not only for the construction activities but also for the administrative expenses.

In line with this, readers may refer to related articles about “Common Formulas for Accounting Ratios ” and “How to Read a Financial Statement” .

There are two ways by which a construction company recognizes income: the “completed-contract” method and the “percentage of completion” method.

Completed Contract

Under the “completed-contract” method, income if any will be recognized only if the project has reached its full completion stage. The cost amounts previously classified as “Work in Progress” are recognized as expenses in order to determine if the total collections from the customer exceed the total expenses.

On the other hand, if the company’s income after project completion decreases, managing the cash flow control of the construction company requires investigating the cause/s of the problem. This is to determine the factors that affect the profitability of the construction project.

Percentage of Completion

Under this method, a portion of the construction work is billed in full to the client. Any amounts received will serve as the construction company’s working capital. Once that particular portion is completed, the books of the construction company recognize the difference between the amount collected and the expenses incurred as its income or loss for a percentage of the project. This method is often preferred as it allows the construction company to manage and control costs and cash flow more easily.

Summary:

Managing cash flow control in a construction project is a complicated process because the activities have to be carefully planned, monitored and matched against the project plans and the budget. The funding for the undertaking should come from the building owner, and improper utilization or inadequate inflow may affect the company’s own cash position if expenses are not carefully monitored.

There are three areas on which the project manager should focus:

- The plan for utilization wherein the budget plans should be strictly implemented because estimates have already taken into consideration the variables.

- The cash flow status report, which provides a summary for monitoring the cash inflows and outflows. Through this report, the manager will be able to perceive at a glance if the budget is being closely implemented and if cash inflow coming from the client is timely and sufficient.

- The company’s financial statement will show that the process of managing the cash flow control in a construction project has implemented the cost controls as planned. It will also disclose fund adequacy or inadequacy – where negative results would prompt the management to thresh-out the matter with the client before proceeding with the project.

Reference and Image Credit Section:

Reference:

- CE - Carnegie Mellon University: 12. Cost Control, Monitoring and Accounting –https://pmbook.ce.cmu.edu/12 _Cost_Control,_Monitoring,_and_Accounting.html

Image Credits:

- Building Under Construction by Conung

- Screenshot images and samples of cost account schedule, cost estimation and cash flow status report were created by the author.