Sunk costs tend to be confusing. In our academic learning, we are taught that they’re necessary but treated as outright losses and hence should be ignored. But will decision makers readily decide on a project without taking into consideration the amount of money regarded as irrecoverable?

The Concept of Taking Calculated Risks

As far as risk management is concerned, sunk expenses should not be ignored for their very essence as irrecoverable costs. The point in time when a decision has to be made should be established before such expenses are regarded as dismissible.

Decisions for projections are based on assessments of potentials and probabilities, including the possible costs that are considered as irrecoverable should a project turn out contrary to expectations. One cannot just go headlong into a project if one is aware that a great part of the money to be invested has a poor or flawed possibility of being recovered. However, it is in determining the net cash increment of the project’s outcome that sunk costs are ignored as part of the cash outflow estimate. That way, a fair value of increment can be gauged against the value of the irrecoverable cost.

Here’s a case study example:

Considering Irrecoverable Cost as a Potential Risk

A company is in the process of deciding whether or not to lease a property in another state; its purpose would be as an extension office. It is needed to reinforce and closely monitor the operations in the region in light of the latter’s current developments. Based on an assessment of the region’s business conditions, an economic boom is bound to take place due to a successful oil drilling exploration .

The current forecast is that about 2,000 new jobs and 500 new businesses will spring from the successful oil drilling exploration. Since the region’s economy is expected to flourish, it has been proposed that a branch office in the region be installed to make the company’s presence felt early on. However, obtaining a property to lease should be done before the anticipated boom takes place, since it is also predicted that the prices of leased properties will rise. The property being considered is for a five-year term at a total lease contract price of $200,000.

At this point, the $200,000 lease contract is regarded as a sunk cost and therefore will not be included in determining the projected net cash increment of the proposed regional office once the economy booms. But it will be considered in its context as a risk to be taken in case business in the region does not improve.

The greater consideration is to ensure that a property can be leased at a lower price than the price that would be offered at a time of economic prosperity. Although there is the risk of incurring an additional $200,000 cash outlay that will burden the present business operations, this cost is pitted against a net increment forecast that has a high potential of being realized.

The concept of sunk cost, therefore, is being considered as part of the risk considerations and not as a component of cost-estimation of the anticipated net increment that will benefit the business. Rather than miss the chance of being among the first to make headway in the region, before the economic benefits fully materialize–it is likely that management will decide in favor of the proposal.

Ignoring Costs That Cannot Be Recovered

In continuing with the case study sample, it came about that during the first year of the lease, the company’s business has not shown any signs of considerable improvement despite the branch office’s establishment in the region. The increment being realized is not as high as had been expected.

It appears that the investors in the oil exploration project have been pulling out their financial support due to rumors that the drilling venture is only a hoax. Hence, the region’s economic boom may take longer or, at worst, may not even take place if the local authorities are able to prove that the exploration is indeed a hoax.

Now there are current suggestions for the company to slash the salaries of the employees in order to ease the cost of the leased property. Others are against this suggestion because the cost of the lease is already considered a loss that is not recoverable. Besides, the company will likewise face additional risks of contending with employment issues and lawsuits , which will only aggravate their current financial position.

It is in this perspective that management will ignore the $200,000 lease contracted, since the cost is a capital investment that cannot be recovered in terms of increments. Accounting-wise, however, the cost is being spread out for a period of five years. This denotes that the loss is also being spread out by matching it against the actual revenue that will be realized annually.

It follows, therefore, that with all other business decisions to be made in running the operation of the regional office, the company should dismiss the idea of recovering the $200,000 in lease costs.

Are Fixed Costs Regarded as Sunk?

There are those who misconstrue fixed costs as falling into the category of irrecoverable costs. In deciding the feasibility of a venture, fixed expenses form part of the projected cash outflow, in order to arrive at the estimated net flow increment. They are not in the same context as the irrecoverable expenses that have to be incurred in order to cross the barriers between entering into a venture and staying engaged in an ordinary activity.

The costs of the research and development team for a product innovation, for example, give management leverage in making decisions. They are regarded as irrecoverable, regardless of the outcome of the research on which decisions to proceed or discontinue the innovation are arrived.

Fixed costs are necessary to make the business venture succeed while sunk costs are necessary to qualify for the venture. Although a fixed cost may be considered as an irretrievable cost because it has to be incurred regardless of the profit to be realized, it is still not equivalent to sunk costs.

If a project has been evaluated by using fixed costs in the same perspective as the sunk expenses, the analysis and evaluation performed is only an assessment of profitability. But if the project has been evaluated and analyzed by taking into consideration the cost that has to be sunk into a contract or into an extraordinary undertaking, then the decision to enter into that project is partly gauged against risks that said costs can no longer be recovered.

References

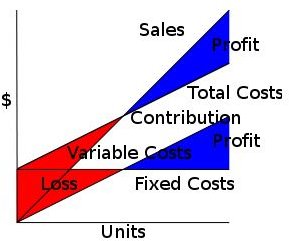

- Image by Nils R. Barth

CVP-TC-FC-VC-Sales-Contrib-VC-PL-compat / at Wikimedia

under public domain - Pindyck, Robert S. Sunk Cost and Real Options in Antitrust Analysis. Massachusetts Institute of Technology at http://web.mit.edu/rpindyck/www/Papers/Vol.%20IChap.%2026CompetitionLaw_m1.pdf

- Image by Albin Martin Zuech,

Director, VA Enterprise Architecture Service

(Retired) Without row-six the Zachman Framework only identifies sunk-cost –

the row-six ROI permits the framework to measure benefits and to be used in a

continuous improvement process, capturing best practices and applying them

back through row-two at Wikimedia under public domain - Image by Guillom Exponential loss Wikimedia CCA Share-Alike License

- Image by Qniemiec – Riskpremium1 / Wikimedia Public Domain

- Economic Decision-Making. Melbourne Businss School. http://www.mbs.edu/home/jgans/mecon/value/Segment%202_2.htm