I had to make a decision. I noted the pros and cons of each possibility. That was not enough! My leadership asked me to calculate the dollars gained or lost by making each decision. It was a project risk management issue. Decision Trees, Expected Monetary Value, Decision Tree Analysis was required.

A Decision Tree Analysis Example

Business or project decisions vary with situations, which in-turn are fraught with threats and opportunities. Calculating the Expected Monetary Value (EMV) of each possible decision path is a way to quantify each decision in monetary terms. Using an EMV decision tree is a recommended Tool and Technique for Quantitative Risk Analysis. For the PMP exam, you need to know how to use Decision Tree Analysis to make decisions in Project Risk Management. In this article, we’ll look at a Decision Tree analysis example. [caption id=“attachment_133141” align=“aligncenter” width=“640”] Risk management is a necessary component of project management[/caption] To understand how to calculate Expected Monetary Value for simple situations, read the Calculating the Expected Monetary Value (EMV)

article.

Risk management is a necessary component of project management[/caption] To understand how to calculate Expected Monetary Value for simple situations, read the Calculating the Expected Monetary Value (EMV)

article.

Steps to Use Decision Trees Analysis

To use Decision Tree Analysis in Project Risk Management, you need to:

- Document a decision in a decision tree.

- Assign a probability of occurrence for the risk pertaining to that decision.

- Assign monetary value of the impact of the risk when it occurs.

- Compute the Expected Monetary Value for each decision path.

The simplest way to understand decision trees is by looking at a Decision Tree analysis example.

Decision Trees Scenario

Suppose your organization is using a legacy software. Some influential stakeholders believe that by upgrading this software your organization can save millions, while others feel that staying with the legacy software is the safest option, even though it is not meeting the current company needs. The stakeholders supporting the upgrade of the software are further split into two factions: those that support buying the new software and those that support building the new software in-house. Confusion reigns in the meeting room with stakeholders pointing out negative risks for each option!!!

Building the Decision Tree

In this scenario, you can either:

-

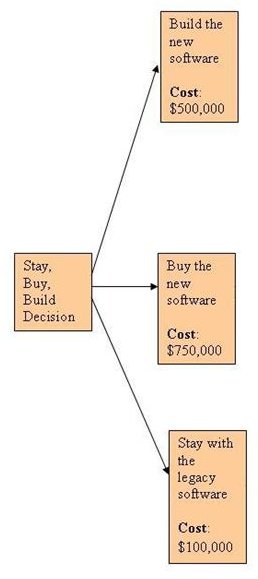

Build the new software: To build the new software, the associated cost is $500,000.

-

Buy the new software: To buy the new software, the associated cost is $750,000.

[caption id="" align=“aligncenter” width=“600”]

Decision Tree Start[/caption]

Decision Tree Start[/caption] -

Stay with the legacy software: If the company decides to stay with the legacy software, the associated cost is mainly maintenance and will amount to $100,000.

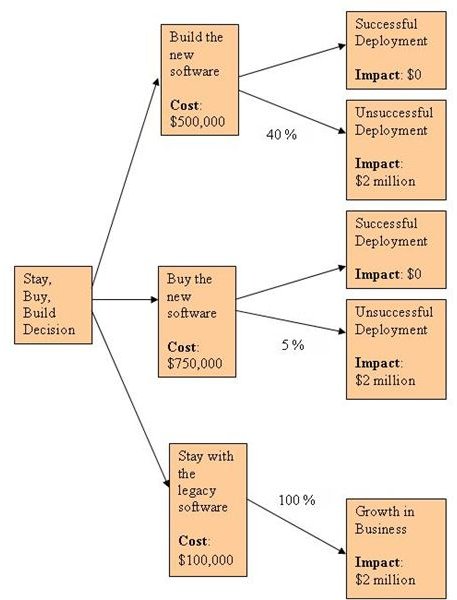

Looking at the options listed above, you can start building the decision trees as shown in the diagram. By looking at this information, the lobby for staying with the legacy software would have the strongest case. But, let’s see how it pans out. Read on. The Buy the New Software and Build the New Software options will lead to either a successful deployment or an unsuccessful one. If the deployment is successful then the impact is zero, because the risk will not have materialized. However, if the deployment is unsuccessful, then the risk will materialize and the impact is $2 million. The Stay with the Legacy Software option will lead to only one impact, which is $2 million, because the legacy software is not currently meeting the needs of the company. Nor, will it meet the needs should there be growth. In this example, we have assumed that the company will have growth.

Calculating Expected Monetary Value for each Decision Tree Path

The diagram depicts the decision tree. Now, you can calculate the Expected Monetary Value for each decision. The Expected Monetary Value associated with each risk is calculated by multiplying the probability of the risk with the impact. By doing this, we get the following:

[caption id="" align=“aligncenter” width=“600”] Decision Tree Complete[/caption]

Decision Tree Complete[/caption]

- Build the new software: $ 2,000,000 * 0.4 = $ 800,000

- Buy the new software: $ 2,000,000 * 0.05 = $ 100,000

- Staying with the legacy software: $ 2,000,000 * 1 = $ 2,000,000

Now, add the setup costs to each Expected Monetary Value:

- Build the new software: $ 500,000 + $ 800,000 = $ 1,300,000

- Buy the new software: $ 750,000 + $ 100,000 = $ 850,000

- Staying with the legacy software: $ 100,000 + $ 2,000,000 = $ 2,100,000

View the image above, to see how all the figures above look like in a Decision Tree after conducting a Decision Tree Analysis.

Decision Trees Example - Making the Decision

Looking at the Expected Monetary Values computed in this Decision Trees example, you can see that buying the new software is actually the most cost efficient option, even though its initial setup cost is the highest. Staying with the legacy software is by far the most expensive option. When you conduct a SWOT Analysis to determine whether a business idea is worth pursuing, there is no quantified data to support your decision. Decision Trees and Decision tree analysis help you quantify the data, which is then useful in convincing stakeholders. It is a critical part in Project Risk Management. Image by mohamed Hassan from Pixabay