What happens when one of the activities goes over budget? How do you mitigate the cost risk associated with critical activities? Reserve Analysis holds the key to these project budget-related answers.

Determining a Project Budget

Reserve Analysis is one of the techniques used to determine a project budget. During Reserve Analysis, a project is analyzed from a cost overruns point of view and buffers are placed in appropriate place. These buffers are called Contingency and Management Reserves.

Contingency and Management Reserves

Contingency Reserves are buffers to account for risks that you know will occur. For example, you may have a Contingency Reserve for lack of the skilled human resources in a certain technology. By looking at the Risk Breakdown Structure , you’ll be able to get more categories that require a contingency reserve. Management Reserves are for risks that have not been identified. Every project is hit by unidentified risks. The Management Reserve protects the project from these critters.

Regardless of the type of reserve, the amount of buffer is proportional to the cost risk foreseen in the project or individual activities. The norms within an organization may also dictate the level of buffering applicable. There is no prescribed method to perform Reserve Analysis. However, the guiding principle is that you should buffer or pad according to the risk levels identified for the project or individual activities. In this article, we’ll use this guiding principle for Reserve Analysis.

Example 1 – Pad Each Activity Cost Estimate

After you’ve created the Precedence Diagram (Network Diagram) for the project and estimated the activity duration and resources, you might realize that the project is very similar to some previous projects that you successfully completed. The risks associated with the project are low and there are no critical pieces that need extra cost buffering. In such a case, you might decide to pad each activity cost estimate by 10 percent across the board. Many organizations have a set policy that will determine the degree of buffering.

Example 2 – Pad High-Risk Activities

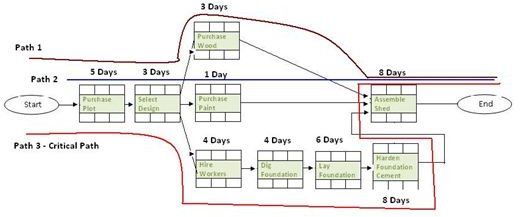

Now, suppose you have identified activities on the critical path and need to give them extra protection. In this case, you would provide a higher

cost buffer to these activities than other activities that are not on the critical path. It is common for the critical path of a project to change during the course of a project. Therefore, it’s safer to pad high risk activities for cost over-run, regardless of whether they are on the critical path or not. For example, you might be developing a non-critical component for a client. If the contract specifies a fixed time, then you may want to utilize an extra cost buffer to ensure schedule crashing , if required, is possible. Alternatively, you may want to pad all activities by 10 percent and the high-risk activities by 20 percent.

Reserve Analysis is not done in isolation to determine the project budget. To read about other techniques, read the Techniques for Determining a Project Cost Budget article.